ISO New England’s 2014 Regional System Plan underscores that retirements indicate the need for new resources to address future demand despite energy efficiency measures projected to flatten demand over time.

On November 6, 2014, ISO New England (ISO-NE) issued the 2014 Regional System Plan, its annual guide on New England’s long term power-system planning efforts. The report provides forecasts of energy and peak demand over a 10-year period and identifies areas of the grid for transmission upgrades and market responses to address reliability requirements. It provides an overview of power system infrastructure, current regional issues, and major initiatives underway. ISO-NE is awaiting final Federal Energy Regulatory Commission (FERC) orders on compliance filings and has requested rehearing on aspects of FERC Order 1000 that would require changes to the regional planning processes.

According to the report, 559 transmission projects – representing $6.6B in new infrastructure investment – were put into service in New England states from 2002 to June 2014. Between November 1997 and April 2014, approximately 15,000 MW of new generation have been constructed and more than 4,100 MW of resources have retired. Demand response and energy efficiency (EE) make up approximately 2,100 MW New England’s resource mix.

The report projects an average one percent annual growth in energy consumption through 2023 – unadjusted for EE measures – and 1.3 percent annual growth in summer peak demand. Projections based on ISO New England’s multistate EE forecast – incorporated in 2012 to capture longer-term EE effects in system planning – show essentially no growth in total electricity usage and 0.7 percent annual growth in summer peak demand over the 10-year period.

The report highlights that ISO-NE has developed the first U.S. multistate forecast of distributed generation (DG) resources to quantify and understand the impact of increased DG on grid operations and planning. The first forecast results show that solar photovoltaic (PV) – the largest segment of New England’s DG – will continue to grow reaching 1,800 MW nameplate capacity by 2023; installed nameplate PV was approximately 500 MW at the end of 2013.

ISO New England expects more than 4,600 MW of capacity to retire over the next three years. Despite the projected slow load-growth, pending large-generator retirements and possibility of additional retirements indicate the need for new capacity resources to address future demand. The eighth Forward Capacity Market auction (FCA) held in February to secure capacity obligations for the 2018/2019 commitment period procured less than the capacity requirement, resulting in higher capacity prices compared to previous auctions.

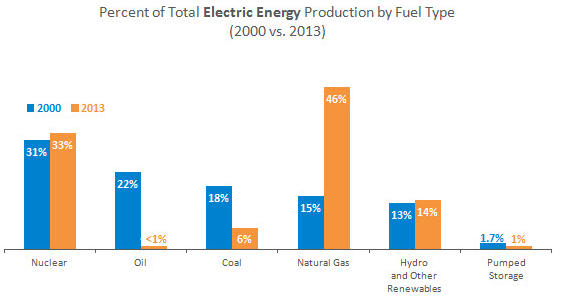

The report notes that approximately $4.5B in transmission investment is planned and several elective transmission projects to be funded by private developers have been proposed. Drawing on November data, the report states that approximately 8,300 MW of new generation has been proposed – more than 4,500 MW of natural gas and approximately 3,700 MW of nameplate wind generation; the proposal queue has had a MW attrition rate of 70 percent. In 2013, natural gas accounted for 45.1 percent of the region’s electricity, oil for less than one percent, coal for 5.6 percent, nuclear for 33.2 percent, and renewable resources for 15.3 percent. Considering system vulnerabilities and limitations indicated during the past two winters and the resultant wholesale electricity price hikes, ISO New England will implement a second Winter Reliability Program to mitigate potential grid reliability issues.

Among the upcoming market enhancements, new market rules set to take effect on December 3 will enable generators to submit power supply offers that vary by hour in the day-ahead market instead of offering one price for the entire operating day. Generators can update real-time market offers to reflect changes in the real-time fuel prices, resulting in more accurate prices and improved resources’ incentives to follow dispatch instructions. Changes to Forward Capacity Market (FCM) elements – approved by FERC in May – set to apply in the February 2015 FCA will facilitate pay-for-performance; they will overcome the current shortcoming of poor resource performance resulting from weakly linked resources’ capacity payments and actual performance. Additionally, beginning with the February 2015 FCA, ISO-NE will implement a sloped-demand curve, a new mechanism to reduce price volatility over time and yield smaller capacity price swings when the market moves from excess supply conditions to periods requiring new capacity resources – likely to occur as resources retire; new resources will have the option of receiving a seven-year lock-in at the clearing price to reduce financial risk for resource developers.

Originally published by EnerKnol.

EnerKnol provides U.S. energy policy research and data services to support investment decisions across all sectors of the energy industry. Headquartered in New York City, EnerKnol is proud to be a NYC ACRE company.