What time is it? Credit: Shutterstock

What time is it? Credit: Shutterstock

Many analysts agree that as US oil companies pullback capital spending, lay down rigs and drill fewer new wells, production will inevitably decline, supply and demand fundamentals will rebalance and oil prices will increase. But that’s where the agreement ends.

International benchmark crude oil prices have recovered a bit from recent lows, but the supply overhang on the global market continues sending bearish signals and weighing on the prospect of significant price recovery. So how long will it take before spending and drilling cutbacks materialize in a physical US oil supply reduction? Let the disagreement begin.

Two separate Bloomberg articles published this week feature starkly differing views on that issue.

“EOG is viewed as the premier company in shale development, and if they’re not going to grow, it is a very important signal to the market,” said Michael Scialla, a Denver-based analyst at Stifel Nicolaus & Co. “The argument that this slowdown is going to take a while to have an impact on supply is completely wrong.” – Bloomberg Business

“You’ve just got a lot of oil and there’s nothing that can be done about this in the short term,” said Bill O’Grady, chief market strategist at Confluence Investment Management in St. Louis, which oversees US$2.4 billion. “Low prices will eventually work their magic and reduce supply, but that takes a lot of time.” – Bloomberg via Financial Post

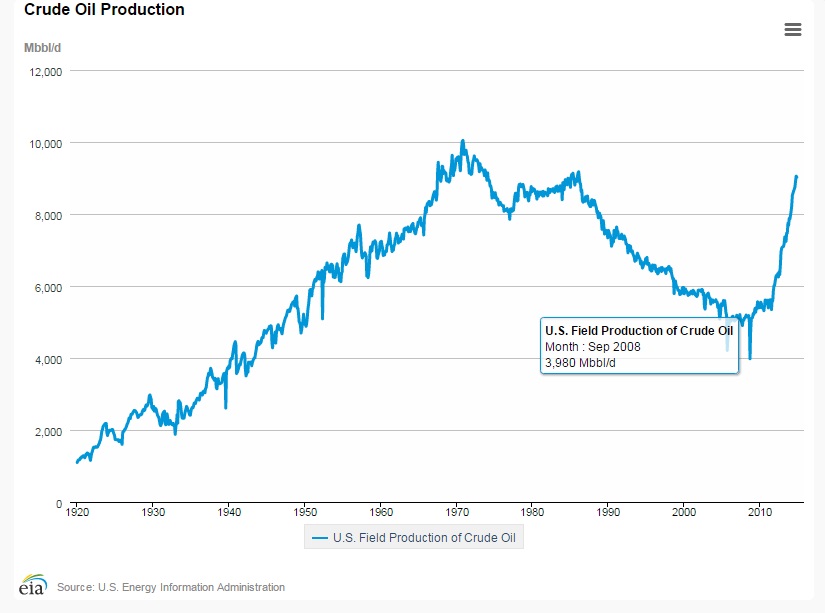

It took 5 months from the time US crude production bottomed out at a little under 4 million barrels per day in September 2008 to when NYMEX WTI futures prices hit their most recent low of $39.26/bbl in February 2009. Prices and production both steadily increased from those points. By February 2010 WTI futures prices had recovered to above $75/bbl.

But the situation is different now. The post-2009 recovery was largely driven by broader global economic growth that increased demand for oil at a time when supply and demand were in closer balance. Now global economic growth alone appears too weak to sop up the surplus oil on the global market.

That’s why all eyes are on US producers and US output. The problem is current estimates anticipate US oil production increasing by about 600,000 b/d in 2015. Slashing that growth estimate to zero would still see the US produce over 9 million b/d of oil this year, which would be a bearish indicator in an otherwise oversupplied market.

So the key – given the way things look right now – is how fast US production growth is erased and total output flattens or even declines. And that is where analysts are arriving at widely divergent views. Ultimately, time will tell and those who guess right stand to profit.