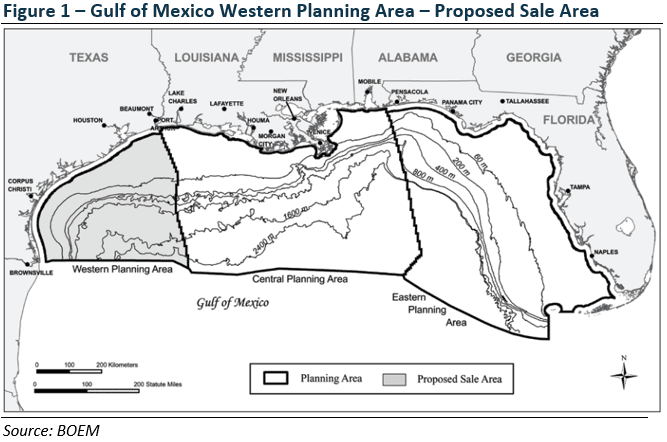

BOEM Lease Sale 246 to Offer all Available Acreage in Western GOM for Oil and Gas Activity

The Gulf of Mexico (GOM) accounts for the majority of oil and gas production on the Outer Continental Shelf (OCS). On March 2, 2015, the Bureau of Ocean Energy Management (BOEM) announced that its proposed Gulf of Mexico (GOM) Lease Sale 246 would offer all available unleased areas in the Western GOM Planning Area for oil and gas activity (Figure 1). Lease Sale 246 – scheduled to take place in New Orleans in August 2015 – would be the eighth offshore lease sale under the OCS 2012-2017 Five-Year Oil and Gas Leasing Program. It will offer approximately 21.8 million acres located 9-250 miles offshore Texas in water depths ranging from 16 to more than 10, 975 feet. The BOEM estimates Lease Sale 246 to result in the production of 116-200 million barrels of oil (MBO) and 538-938 billion cubic feet (Bcf) of natural gas.

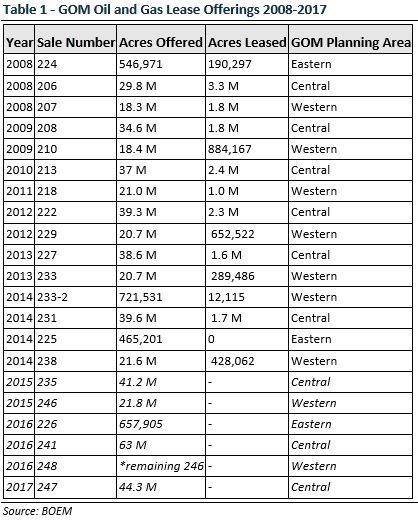

Lease sale 246 will build on the more than 13.5 million acres already sold through lease auctions during President Obama’s time in office (Table 1).

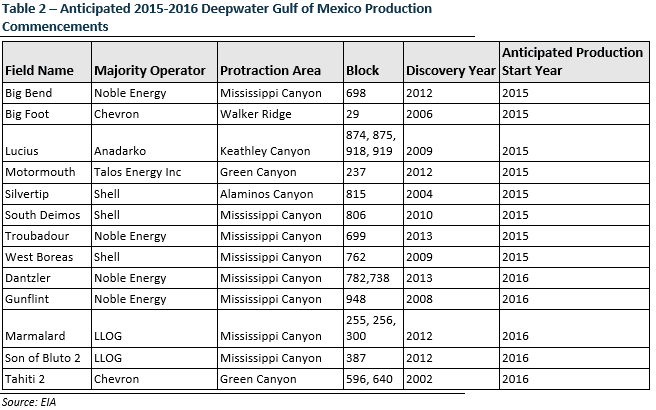

Recent Upturn in GOM Oil and Gas Activity Reflects Resurgence of Deepwater Drilling

GOM projects started in 2014 and those scheduled for 2015-2016 outpace the 2011-2013 period. Thirteen fields are expected to begin production in 2015 and 2016 alone (Table 2). The upturn reflects renewed interest in GOM oil and gas activity following the temporary deepwater drilling moratorium that lasted from April 30-October 12, 2010, in response to the 2010 Deepwater Horizon incident. Deepwater projects that began operations in 2014 include (by majority operator):

- Stone Energy – Cardamom Deep

- Stone Energy – Cardona projects

- Chevron – Jack/St. Malo fields

- Murphy Oil – Dalmatian

- Hess – Tubular Bells

Proposed 2017-2022 Five-Year Program Prioritizes GOM Development over Alaskan, Atlantic, and Pacific Areas

The proposed 2017-2022 offshore lease program is projected to unlock approximately 80 percent of estimated undiscovered technically recoverable oil and gas resources on the OCS. The Outer Continental Shelf Lands Act authorizes the Department of the Interior (DOI) to grant mineral leases and govern oil and natural gas activities on OCS lands. It requires DOI to prepare a five-year program detailing a schedule of lease sales and proposed leasing activity that best meets the national energy needs while addressing economic, environmental, and social considerations. OnJanuary 27, DOI announced the Draft Proposed Program (DPP) for 2017-2022. The DPP includes eight planning areas – three in the Gulf of Mexico, two in the Atlantic, and three in Alaska. It schedules 14 potential lease sales for the five-year period– 10 sales in the Gulf of Mexico, one in the Atlantic, and three off the Alaskan coast.

On March 9, a group of 12 Senators urged DOI to exclude Atlantic oil and gas leasing from its 2017-2022 program, intending to protect the states of Virginia, North Carolina, South Carolina, and Georgia from potential incidents similar to the 2010 Deepwater Horizon oil spill.

Also, despite the president’s broad offshore oil and gas development support, on January 27, he designated 9.8 million acres in the Beaufort and Chukchi Seas as off-limits to consideration for future oil and gas leasing. The designation would block oil drilling efforts in the Coastal Plain region estimated to contain about 7.7 billion barrels of oil (BBO). It could also impact future proposed offshore oil and gas lease sales in the Beaufort Sea, which is estimated to hold approximately 7.2 BBO. If Congress passes the policy, it would result in the largest wilderness designation since the Wilderness Act of 1964.

Central and Western GOM Planning Areas are the primary offshore sources of U.S. oil and gas

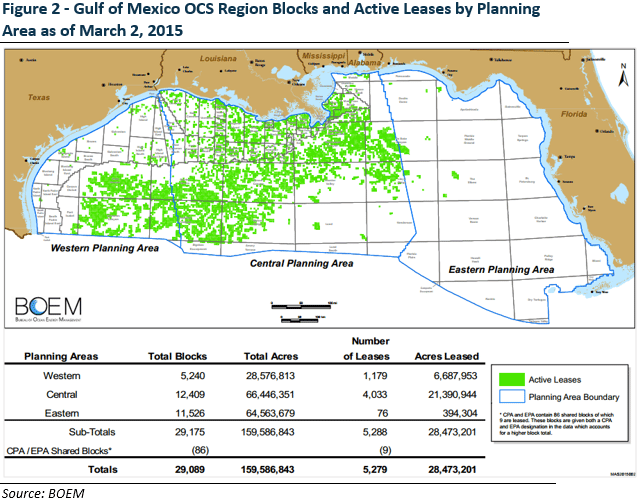

The GOM Region contains approximately 160 million acres in three planning areas. The GOM’s Central and Western GOM Planning Areas offshore of Alabama, Mississippi, Louisiana, and Texas, form the primary offshore source of domestic oil and gas, generating approximately 97 percent of all OCS oil and gas production. Although much of the Eastern GOM Planning Area is unavailable for leasing through June 30, 2022, there are existing leases in all three planning areas. Currently, the majority of the Eastern GOM Planning Area and a small portion of the Central GOM Planning Area are unavailable through FY 2022, as part of the 2006 Gulf of Mexico Energy Security Act (GOMESA).

The GOMESA also provides for sharing offshore oil and gas lease revenues — bonuses, royalties, rentals, and corporate income tax – with the four Gulf producing states and their coastal political subdivisions. GOMESA Phase I – began in FY 2007 – provides 37.5 percent of qualified revenues for sharing and allocates 12.5 percent to the Land and Water Conservation Fund. Phase II – which begins in FY 2017 – applies a $500M/year revenue sharing cap from FY 2016 through FY 2055 and expands the definition of qualified revenues.

In FY 2014, the GOM provided the bulk of the $13.5B offshore and onshore energy revenue, supplying approximately 18 percent of U.S. oil and 5 percent of gas production. Similar metrics were achieved in 2013. The six sales held under the current five-year program have yielded approximately $2.4B in auction proceeds. Currently, the OCS has approximately 6,000 active leases, spanning more than 32 million acres – the vast majority in the GOM (Figure 2), and the remainder in Alaska and Pacific regions.

Subsea Tieback Technologies Support Production Increases

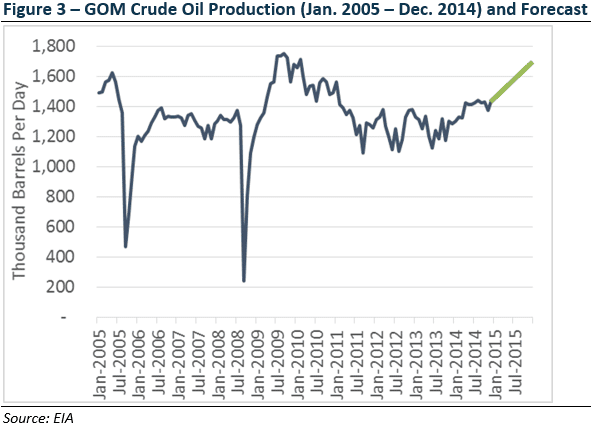

High surface structure costs associated with offshore oil field development make only large field developments economical. Reserves that are not sufficiently large to justify such investment use the somewhat recently introduced subsea tiebacks technology – a method that connects subsea infrastructure to nearby existing platforms – thereby reducing costs and well start-up times. The EIA notes that more than 50 percent of projects scheduled to start in 2015 and 2016 will use subsea tiebacks. These projects combined with those that came online in 2014 are expected to add approximately 265,000 barrels per day (bbl/d) by the end of 2015 (Figure 3). The EIA production estimates include adjustments for potential seasonal shut-ins from hurricanes. The EIA’s mean estimate of GOM offshore production outages during the 2014 hurricane season totals 12 Mbbl of crude oil and 30 billion cubic feet (Bcf) of natural gas.

Producers Collaborate to Increase Offshore Project Cost-Effectiveness

The current oil price decline increases the uncertainty of deepwater project timelines, posing early stage projects to risks of delay. To address this issue, producers are engaging cost-sharing and other collaborative efforts to shorten the time between final investment decision and first production. In January Chevron Corporation announced a collaboration with BP Exploration and Production and ConocoPhillips Company to explore and appraise 24 jointly-held offshore leases in the Keathley Canyon. The joint effort aims to achieve scheduling efficiencies, cost savings, and resource optimization. Centralized production efforts similar to Chevron’s Jack/St. Malo project also aim to improve capital efficiency. The Jack and St. Malo fields, which began production in December 2014, are expected to ramp up production over the next few years to a total daily rate of 94,000 bbl of oil and 21 Mcf of natural gas. These fields have more than 30-year planned production lives, and are expected to recover in excess of 500 million oil-equivalent barrels by using current enhanced recovery technologies.

Insight to Industry – Despite Low Oil Prices, GOM is Well-Positioned for Increased Offshore Oil and Gas Activity

Renewed industry interest – evident from the recent upturn in GOM projects – and the DOI’s priority for GOM development in its proposed 2017-2022 program will help revive the region’s offshore oil and gas production. Due to the lengthy timelines associated with deepwater projects, market fluctuations are likely to have minimal impact on GOM projects in mid- to late-state development. However, the recent oil price decline adds uncertainty to GOM projects still in early development stages.

In addition to domestic offshore development, partnerships may begin at the U.S.-Mexico border. Mexico made constitutional amendments in December 2013 and enacted secondary legislation in August 2014 that opened oil and natural gas markets to foreign investments, including investments that are active in the GOM OCS. Opening of Mexican waters could facilitate long-term expansion of U.S.-Mexico energy trade and provide opportunities for U.S. companies, while there is a possibility for a shift in investment focus from the U.S. OCS to Mexican waters.

Originally published by EnerKnol.

EnerKnol provides U.S. energy policy research and data services to support investment decisions across all sectors of the energy industry. Headquartered in New York City, EnerKnol is proud to be a NYC ACRE company.